Why FD Rates Matter Right Now

The Reserve Bank of India has kept the repo rate steady this cycle, which means deposit rates have mostly stabilized rather than dropping sharply like they did through 2025. That stability is actually good news for savers — it means the current rates are likely to hold for a while, giving you a reliable window to lock in a good return.

Top FD Rates Across Bank Categories (June 2026)

Small Finance Banks — Highest Returns

Small finance banks consistently offer the best FD rates because they need to attract deposits more aggressively than large national banks. They’re still RBI-regulated and your deposits remain insured up to ₹5 lakh under DICGC, making them a genuinely safe option despite being smaller institutions.

| Bank | Highest Rate (General) | Highest Rate (Senior Citizen) | Best Tenure |

|---|---|---|---|

| Unity Small Finance Bank | 7.80% | 8.30% | 501 days |

| Suryoday Small Finance Bank | 8.10% | 8.60% | Select tenures |

| Utkarsh Small Finance Bank | 8.10% | 8.60% | Select tenures |

| Equitas Small Finance Bank | 7.75% | 8.25% | 888 days |

| Shivalik Small Finance Bank | 7.80% | 8.30% | Select tenures |

Major Private & Public Sector Banks — Stability First

If you prefer the comfort of a well-known, large-scale bank, here’s where the major names stand this month:

| Bank | Highest Rate (General) | Notes |

|---|---|---|

| HDFC Bank | 7.40% | Stable, widely trusted |

| SBI | 6.50% | India’s largest bank, lowest risk perception |

| ICICI Bank | ~7.00% | Competitive on mid-tenure deposits |

| Punjab & Sind Bank | 6.75% | Highest among PSU banks, 666-day tenure |

Foreign Banks — Lower Rates, Niche Use

Foreign banks operating in India generally offer lower FD rates and are best suited for NRI banking needs rather than maximizing returns. Deutsche Bank tops this category at 7.00% for one-to-two-year deposits, with Standard Chartered and HSBC trailing behind.

Small Finance Bank FD vs Big Bank FD — Which Should You Choose?

This is the question most people get stuck on, so let’s break it down simply.

Choose a small finance bank FD if:

- You want the highest possible return

- Your deposit amount is under ₹5 lakh per bank (so it’s fully DICGC-insured)

- You’re comfortable with a slightly less-known brand name

Choose a big bank FD if:

- You’re depositing a large amount and want maximum brand trust

- You value easy access to branches and customer service

- You’re risk-averse and prefer well-established institutions, even at a lower rate

A smart middle-ground strategy many investors use: split your FD investment across 2–3 small finance banks (keeping each under ₹5 lakh) to maximize both returns and insurance coverage.

How Much Will You Actually Earn?

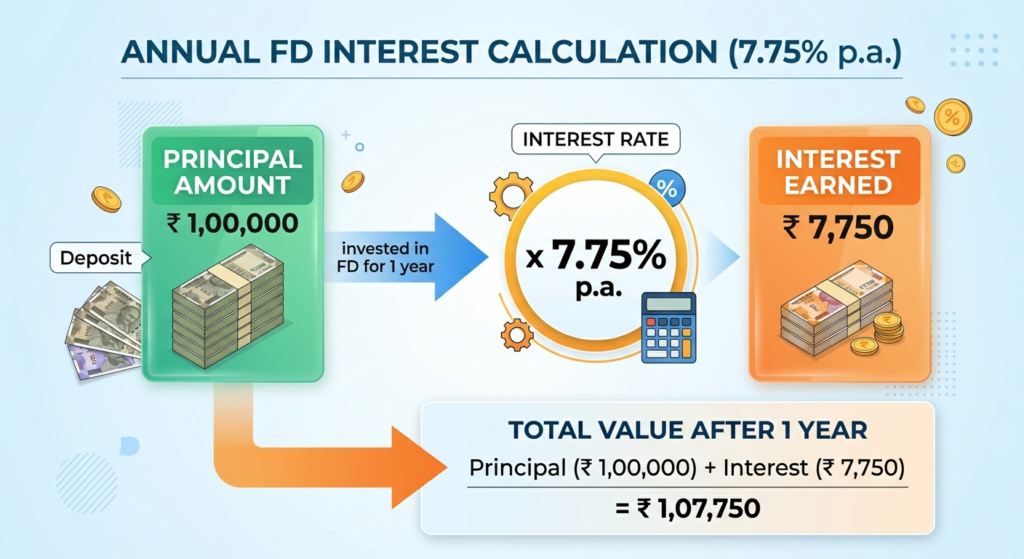

Here’s a simple example using a 1-year FD:

If you invest ₹1,00,000 in a small finance bank FD at 7.75% for one year, you’ll earn approximately ₹7,750 in interest (before tax deduction). The same amount in an SBI FD at 6.50% would earn you roughly ₹6,500 — a difference of over ₹1,200 for the exact same risk-free deposit.

Over a 5-year tenure with compounding, that gap widens significantly, which is why comparing rates before locking in your money genuinely matters.

A Few Things to Check Before You Invest

- TDS applies if your interest income crosses ₹40,000 in a year (₹50,000 for senior citizens). Plan for this at tax time.

- Premature withdrawal penalties typically range from 0.5% to 1% — confirm this before locking in a long tenure.

- Cumulative vs non-cumulative FDs — cumulative FDs pay interest at maturity (better for compounding), while non-cumulative FDs pay out monthly or quarterly (better if you need regular income).

- Always stay under ₹5 lakh per bank if you’re choosing small finance banks, to remain fully covered under deposit insurance.

Final Take

If safety is your only priority and you don’t mind the lower return, SBI or HDFC remain solid choices. But if you’re comfortable with RBI-regulated small finance banks and want meaningfully higher returns on the same risk-free FD structure, banks like Suryoday, Utkarsh, and Unity Small Finance Bank are currently offering some of the best rates available in the market.

As always, rates change frequently — confirm the latest numbers directly on the bank’s website or app before booking your FD.

Which bank are you considering for your next FD? Let us know in the comments.

Related reads you might like:

- Smart Investment Strategies for Beginners to Build Wealth in 2026

- How to Build an Emergency Fund in India