The Wealth Transfer Tsunami Nobody's Talking About

Your parents worked their entire lives to build assets. A house. A business. Investments. Insurance policies. And one day, you'll inherit all of it.

Here's what most Indians don't know: ₹83 trillion worth of wealth will transfer from parents to children across India in the next 20 years. That number isn't a guess — it's from UBS's 2025 wealth projection report. And starting in 2026, this tsunami is officially happening.

But here's the catch that keeps families up at night.

Most Indians think: "If there's no inheritance tax in India, I keep everything tax-free, right?"

Wrong.

Your parents might have already paid income tax on that money. The asset might gain value while you own it. You might have to pay capital gains tax when you sell it. And if your parents made a mistake in their will or the asset transfer, you could lose thousands to legal fees.

This isn't a post about depressing tax laws. This is about the 5 legal moves that will keep lakhs in your family's pocket instead of the government's.

Let's start with what you actually need to know.

Part 1: The (Surprisingly Good) News — What You DON'T Have to Pay Tax On

India does not have an inheritance tax. This is genuinely rare globally — most developed countries do.

So if your parent dies and leaves you their house, their car, their jewelry, their bank accounts — you don't pay any tax on receiving it.

That money moves directly to you. Tax-free. No government cut.

This is why wealth transfers in India are so powerful. Your parents already paid income tax when they earned it. You don't pay again when you receive it.

But— and this matters — you inherit both the asset and any tax liabilities tied to it.

Here's where people stumble.

Part 2: Where the Tax Actually Hits (And It's Not Where You Think)

The Three Hidden Tax Traps

Trap 1: Capital Gains Tax When You Sell

Your parent bought a rental property in 2000 for ₹10 lakh. In 2026, it's worth ₹80 lakh. They pass away and leave it to you.

You inherit it tax-free. But here's the problem:

When you sell it 2 years later for ₹90 lakh, you'll pay capital gains tax on the entire ₹80 lakh profit (from ₹10 lakh purchase to ₹90 lakh sale).

Wait — shouldn't that profit be split between what your parent earned and what you earned?

It should, but it's not. India's tax law gives you a "step-up in cost basis" on death. Meaning: whatever the asset was worth on the day they died becomes your new starting price for tax purposes.

So your actual taxable gain is only ₹10 lakh (from ₹80 lakh inherited value to ₹90 lakh sale price), not ₹80 lakh. You'd pay capital gains tax on ₹10 lakh — roughly ₹2-3 lakh depending on your tax slab.

This is actually good news. Most countries don't give this break. But you only get it if you're aware of it.

Trap 2: Rental Income on Inherited Property

Inherited a rental property? Any rent you collect is treated as your income. Tax as normal.

Your parent collected ₹30,000/month in rent. Now you do. You'll file it in your income tax return. This is straightforward, but many inheritors are shocked when they realize inherited income still gets taxed.

Trap 3: Undisclosed Family Loans Become Gifts (And Gifts Get Taxed)

Here's a weird one that catches families.

Your parent gave you ₹5 lakh "as a loan" 10 years ago. You never documented it. They never asked for it back. Now they've died and their will says you inherit another ₹20 lakh.

The income tax department might look at that undocumented ₹5 lakh and reclassify it as a gift. And gifts above ₹50,000 in a financial year from anyone (even family) are taxable.

This rarely happens, but it's a risk if your family has undocumented transfers.

Part 3: The 5 Legal Moves That Save Lakhs (Your Parents Should Do NOW)

If your parents are still alive, they can implement these moves to make your inheritance smoother and cheaper. If they've already passed, some of these still apply to your planning.

Move 1: Create a Proper Will (This One's Non-Negotiable)

A will costs ₹500-5,000 to make. Probate fees (if needed) run ₹100-500 per ₹1 lakh of asset value.

Without a will, your inheritance goes through "intestate succession" — a legal process that takes 2-3 years and costs significantly more.

Worse: your parents' assets might be divided not how they wanted, but how the law says. A widow, son, and daughter might all fight over the house. Everyone loses. The state wins.

Cost of no will: ₹2-10 lakh in legal fees + 2-3 years of family stress. Cost of a proper will: ₹5,000.

Do the math.

Move 2: Register Major Assets in Both Names (For Married Couples)

If your parent owns a house, property, or business alone, the moment they die, that asset needs to go through probate to transfer to you.

If your parent and spouse own it jointly with right of survivorship, the spouse becomes the owner automatically. No court. No delay. No fees.

Then they can pass it to you via a simpler process or another will.

This is especially powerful for real estate. A joint ownership deed with your spouse means your kids avoid legal tangles.

Move 3: Maintain Meticulous Records of All Assets

Your parent has investments, FDs, properties, jewelry, insurance policies. Write them all down.

For each asset, document:

- What it is (property address, FD certificate number, etc.)

- Original purchase price and date

- Current estimated value

- Where the document is located

Why? When you inherit the property and later sell it, you'll need the original purchase price to calculate capital gains. If the document is lost, you'll spend ₹20,000 to get a certified copy from the property registry. Or worse, you'll lose the cost basis entirely and pay tax on the entire sale price.

Action item: Create a simple spreadsheet right now. One parent per row. One column per asset type. Store it securely.

Move 4: Plan for Illiquid Assets (The House Problem)

Your parent passes away and leaves you a house worth ₹1 crore. You inherit it tax-free. Wonderful.

But you need ₹15 lakh for your child's education. You can't pay it with a house.

Your options:

- Sell the house (capital gains tax applies, even at a loss in some cases)

- Take a loan against the house (you pay interest)

- Let your parents help by setting aside liquid assets in their will specifically for "inheritor cash needs"

Many parents don't think about this. They leave everything in real estate or illiquid businesses. Their children inherit ₹1 crore in assets but ₹0 in cash, and end up selling at a loss just to pay expenses.

Solution: If your parents have ₹50 lakh in property and ₹10 lakh in savings, they should leave at least ₹5 lakh in a bank account or FD specifically for you to cover immediate expenses after they're gone.

Move 5: File for Life Insurance Claims Immediately

If your parent had life insurance, the claims process is separate from the will.

Life insurance payouts go directly to the nominated beneficiary — usually the spouse or children — and bypass probate entirely. It's tax-free income.

Most families miss this because:

- They don't know the policy exists

- They forget to file within 6 months of death

- They wait for probate to finish before claiming (unnecessary)

Action: Find all life insurance policies now. Confirm you're listed as a nominee. When the time comes, file a claim immediately with the company. You'll get the money in 20-30 days, not 2-3 years.

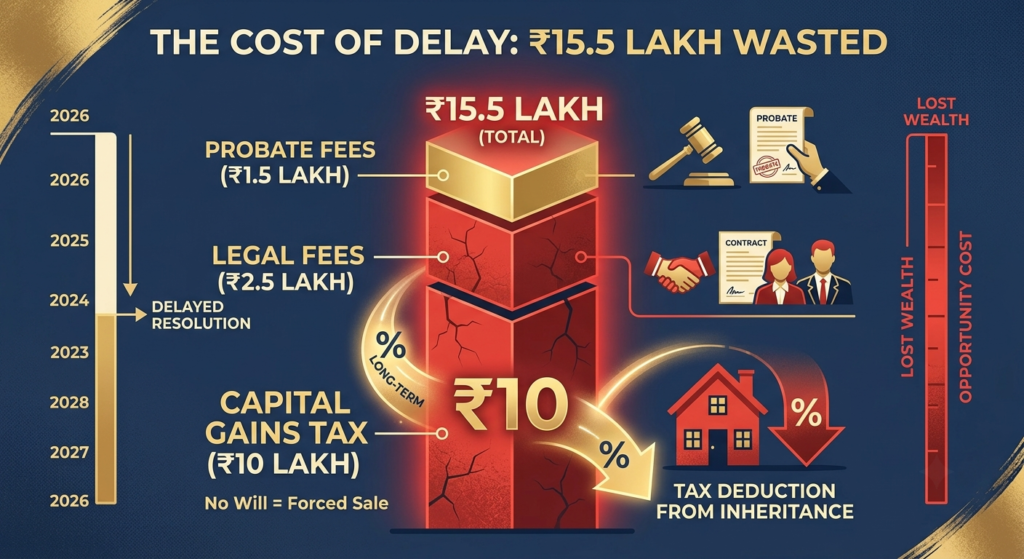

Part 4: What Happens If You Ignore This (A Real Story)

Two brothers, Rajesh and Vikram, inherited a rental property worth ₹80 lakh from their father in 2023.

Their father had bought it for ₹8 lakh in 1995. He'd collected rent on it for 25 years but never registered the property officially in both names with their mother.

When he died:

- The property went through probate (2 years of court dates, ₹1.5 lakh in legal fees)

- The mother had to hire a lawyer to claim her share (₹50,000)

- A dispute arose over whether one son got more shares than the other (unnecessary drama, ₹2 lakh in mediation costs)

- When Rajesh finally sold his half for ₹45 lakh in 2025, he had to pay capital gains tax on the entire ₹45 lakh because the cost basis wasn't properly documented (nearly ₹10 lakh in tax)

Total damage: ₹15.5 lakh in costs and taxes that could've been entirely avoided with proper planning.

If their father had:

- Made a clear will

- Registered the property jointly with the mother

- Kept proper purchase documentation

- Set aside liquid assets for probate costs

They would have saved ₹15 lakh and 2 years of family stress.

Part 5: The Practical Checklist (For Right Now)

If Your Parents Are Alive:

- Have them create or update their will this month

- Register major assets (house, business) in joint names with right of survivorship

- Get a comprehensive list of all assets, with original purchase prices

- Make sure you're listed as a beneficiary on life insurance and bank accounts

- Have a conversation about their wishes — where things go, who gets what, why

- Set aside 10-20% of liquid assets specifically for probate and immediate expenses

If Your Parent Has Recently Passed:

- File life insurance claims within 6 months

- Get the will probated immediately (don't delay)

- Collect all original purchase documents for inherited property

- Track the date of death valuation for capital gains tax purposes

- If you'll sell inherited property, wait at least 2-3 years to minimize gains tax

- Hire a good CA if the estate is complex (cost: ₹10,000-50,000; savings: often ₹3-5 lakh)

If You're Planning Your Own Wealth Transfer (To Your Kids):

- Make a will, even if you think you have time

- Register property jointly with your spouse

- Keep clear financial records in a family safe or locked drawer

- Leave a list of passwords and account numbers with your will

- Document the "why" — write a family letter explaining your wishes

- Review your will every 5 years or after major life changes

The Bottom Line: This Matters Now

₹83 trillion in wealth transfers happen in the next 20 years.

Your family is part of that number. Whether you're the one passing wealth or receiving it, the next 6 months are critical.

A 30-minute conversation with your parents about their will could save you ₹10 lakh and 2 years of family drama.

A simple ₹5,000 will could prevent ₹2 lakh in legal fees.

Proper documentation could save you 20% on capital gains taxes when you eventually sell inherited property.

Most Indians don't plan for this until it's too late. Their kids end up scrambling, selling assets at a loss, paying unnecessary taxes, and fighting with siblings.

You now know better.

This week: Have one conversation with your parents about their will. Next week: Get it done. That's it.

Your future self will thank you.

Related Articles You Should Read:

- How to Start a SIP in India in 2026 — A Step-by-Step Beginner's Guide

- Groww vs Zerodha vs Paytm Money: Which Platform Should You Use in 2026?

- FD Interest Rates June 2026: Which Bank Gives You the Highest Returns?

- Smart Investment Strategies for Beginners to Build Wealth in 2026

Disclaimer: This article is for educational purposes only and does not constitute legal or financial advice. Wealth transfer, inheritance, and tax planning are complex and vary by individual circumstances. Consult a SEBI-registered financial advisor and a qualified tax lawyer or Chartered Accountant before making any decisions regarding inheritance or wealth transfer. Laws can change, and this information reflects 2026 regulations.

Leave a Reply